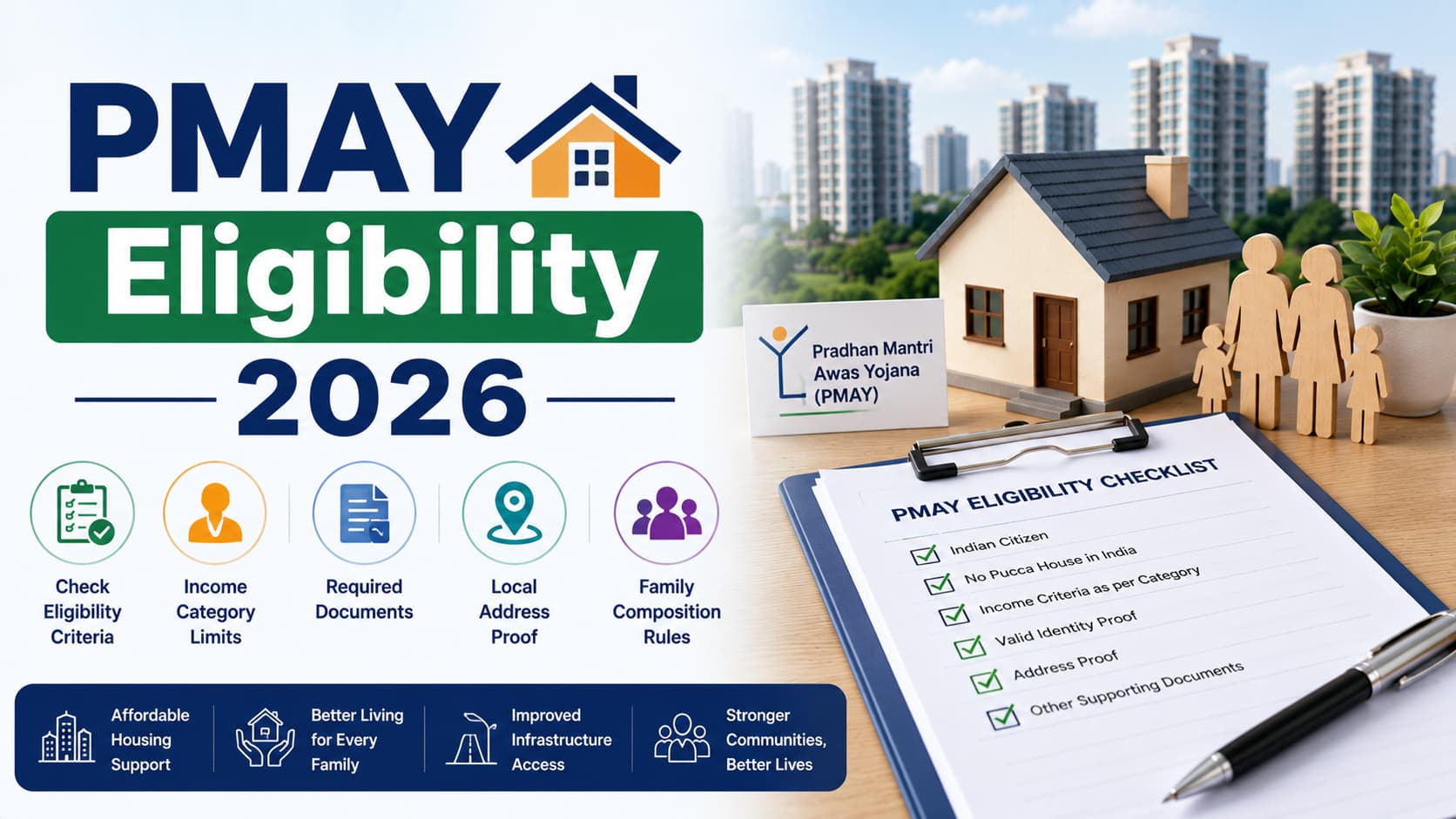

PMAY Eligibility 2026: Who Actually Qualifies for Pradhan Mantri Awas Yojana

Pradhan Mantri Awas Yojana is the biggest housing subsidy scheme in the country, and the one thing that most buyers end up learning about it is the fact that they are ineligible. Not because the requirements are complex. But because they’re paradoxical. Buyers are ineligible if they own a piece of their ancestral land that they’ve never even set eyes on. They are ineligible if the couple consists of a man who inherited a portion of his family’s property back in 1998. The subsidy amount is capped at an area of carpet that most buyers end up exceeding inadvertently, and it mandates the presence of a female co-owner in one particular eligibility category that most applicants believe is non-compulsory.

This article talks about PMAY Eligibility as it really stands in 2026 – the income ranges, the property ownership criteria, the carpet area requirements, the woman ownership clause, and the application rejection causes.

What PMAY Is, and What Changed

The scheme was rolled out in 2015 with both PMAY-Urban and PMAY-Gramin branches. The CLSS (Credit Linked Subsidy Scheme) was the main instrument in both cases, providing a subsidized interest upfront credited to your home loan account and decreasing the principal.

The PMAY-U 1.0 application deadline was on 31 December 2024, while the CLSS instrument itself for EWS/LIG category lapsed in March 2022, and for MIG-I and MIG-II categories lapsed in March 2021.

PMAY-Urban 2.0 received the Cabinet approval in August 2024 with the budget of ₹10 lakh crore and aiming at one crore urban families in five years. It's the current scheme, and its design is different from 1.0.

If you see in guides references to MIG-II slab and ₹2.35 lakh subsidy, you are dealing with a scheme which does not accept applications anymore.

PMAY-U 2.0: The Four Verticals

The new program covers four verticals that operate individually. Depending on which one fits your profile will decide everything.

Beneficiary-led Construction (BLC). It is applicable to individuals who own land plots where they wish to construct homes. Centrally subsidized up to ₹2.5 lakh, with additional state subsidy.

Affordable Housing in Partnership (AHP). Affordable housing constructed by public/private developers, to be sold to qualified beneficiaries. Centrally subsidized up to ₹2.5 lakh per unit.

Affordable Rental Housing (ARH). It covers rental units meant for migrants, women workers and industrial workers. There is no individual subsidy, only the subsidy is provided to the developer/operator.

Interest Subsidy Scheme (ISS). It replaces CLSS and is what many homeowners would be interested in. Interest subsidy on housing loans up to ₹25 lakh, for house costing up to ₹35 lakh.

In comparison with the previous CLSS, the interest subsidy scheme appears to be a little more rigid. The subsidy of 4% can be claimed from the first ₹8 lakh of loan, up to ₹25 lakh, with maximum benefit of ₹1.80 lakh, payable at 5-year intervals over 12 years through button push system.

Compare that to CLSS under 1.0, where an EWS/LIG borrower could receive ₹2.67 lakh upfront and an MIG-I borrower ₹2.35 lakh. The new scheme is more targeted and less generous per household — which is what happens when you're trying to reach a crore of them.

PMAY Eligibility: The Income Slabs

Income determines your category, and the category determines your entitlement.

Under PMAY-U 2.0, the MIG slab has been consolidated. The old MIG-I (₹6–12 lakh) and MIG-II (₹12–18 lakh) split from 1.0 is gone, and the ceiling has come down to ₹9 lakh.

That's a significant tightening. Households earning ₹15 lakh who would have qualified under MIG-II in 2020 are outside the scheme entirely in 2026.

What Counts as "Household Income"

This is where applications quietly fail.

Household income means the combined annual income of the entire beneficiary family — not the applicant's salary. That includes:

The applicant's income

The spouse's income

Income of unmarried children

Rental income from any property

Agricultural income

Interest, dividends, and business income

A couple earning ₹5 lakhs each per annum makes a household of ₹10 lakhs but is out of MIG ceiling limit although both fall under the LIG category individually.

Incomes are evaluated through self-certification in most instances, based on ITRs, Form 16, or self-declaration for unorganized sectors' workers. However, self-certification does not mean license.

Misdeclaration entails subsidy recovery with interest, and lending agencies conduct cross-referencing through ITRs and banking details while issuing loans.

The Property Ownership Bar — Where Most People Fail

Read this very carefully, because it is the most important clause in the entire scheme and is the least understood.

The beneficiary family should have no pucca house anywhere in India in the name of any family member.

Nowhere in the city where you are purchasing. Nowhere in India.

The beneficiary family consists of husband, wife and unmarried children. Adult earning children, whether married or unmarried can form separate families.

The criteria which will get you disqualified:

Your share of an inherited property. Inheriting a quarter share of the ancestral property, in your hometown, which is a pucca house owned by the family member. Disqualifies you even if you haven’t set foot in there in a decade.

A house registered in your wife’s name. The family is a joint family. The flat she owns in Coimbatore disqualifies your purchase in Pune.

A house which you have rented out but do not reside in yourself. Occupancy does not matter; it is ownership that matters.

If you have received a house under some previous housing schemes of the government. Explicitly stated. Being disqualified for having used the scheme IAY, RAY and PMAY 1.0 is permanent.

What does not disqualify:

Possession of vacant land without a pucca house.

It is none other than for whom the BLC vertical stands.

A kutcha or semi-pucca house, even though different states have their own definitions

Ownership of a house by an adult married son who forms his own family unit

Ownership of a house by the parents without being a joint owner of your own family unit

The distinction between owning a plot and owning a house is fundamental, and it's the reason two families in identical financial positions get opposite answers.

The Woman Ownership Requirement

Under EWS and LIG category, the property is to be held by an adult female member of the household.

Not Preferred. Mandatory.

However, an exemption from this requirement is allowed if there are no adult females in the household. While under MIG category, the requirement is more flexible and only sole possession by a man is restricted.

This may well be the most significant silent feature of the program. Millions of properties have come into the names of women in households where that was not likely to happen under any circumstances.

It also works very well with stamp duties. Delhi provides women 4% against 6% for men. Haryana provides women 5% against 7%. Gujarat waives off stamp duty for women who purchase property in their names. Any eligible family under PMAY falling in either EWS or LIG category will automatically satisfy the stamp duty discount.

One needs to remember the caveat in the process - Ownership should be legitimate with proper documentation of contribution, else clubbing provision under Section 64(1)(iv) and benami comes into picture.

Carpet Area — Not Built-Up, Not Super Built-Up

Carpet area is the usable space within the perimeters of the walls of the unit. This doesn’t include the external walls of the unit, the balcony, the service shaft, and the common areas.

Cap under PMAY-U 2.0: 30 sq m for EWS, 60 sq m for LIG, 120 sq m for MIG.

Buyers often confuse the wrong figures. An apartment with a carpet area of 120 sq m is around 155-165 sq m built-up area and 175-190 sq m super built-up area – let’s say 1,900 to 2,050 sq ft for marketing purposes. Super built-up area is what developers promote whereas the scheme considers carpet area.

RERA insists that carpet area is declared in the agreement of sale. Look at the RERA declaration; don’t go by the brochure.

Going above the cap doesn’t lower your subsidy amount; it will just make you ineligible for the subsidy.

Location and Documentation

Location. It should be in a statutory town as per Census 2011, or in a notified planning area by the respective state government. Peri-urban areas, which are not in the notified planning area, are not eligible for PMAY-U but can apply for PMAY-Gramin.

Aadhaar. All members of the family must have Aadhar. It is mandatory and non-negotiable because it is the process through which duplication is detected.

Documents required:

Aadhaar of all family members

PAN of the Applicant

Income Proof – ITR, Form 16, Salary slips or Self Declaration

Six Months Bank Statements

Property Certificate – Allotment Letter, Agreement for Sale, or Title Deed

Self-declaration about no pucca house property ownership in any part of India

Caste Certificate in case of reservation claim under SC/ST/OBC category

Disability Certificate, in case of disability

Loan Sanction Letter of the Primary Lending Institution

How to Apply

Step 1 – Be honest in determining eligibility. Test the income criterion on household income. Test the ownership criterion across all members and states. Test carpet area criterion against RERA.

Step 2 – Apply on the PMAY-U 2.0 portal. Registration takes place at pmay-urban.gov.in. Aadhaar based verification followed by household and income information.

Step 3 – Apply through a Primary Lending Institution. For the ISS vertical, the subsidy comes through your lending institution. Scheduled Commercial Banks, Housing Finance Companies, Regional Rural Banks and Cooperative Banks have been empanelled for this purpose. The lending institution verifies eligibility and submits the application to the Central Nodal Agency – NHB, HUDCO or SBI.

Step 4 – Track. Applications can be tracked either by the assessment ID or by Aadhaar on the portal.

Step 5 – Receive. As per the ISS vertical, the subsidy will come through in five year instalments over a 12 year loan period using the push button method. This differs from the CLSS vertical where a one time credit was made under 1.0.

Beware of consultants charging fees to "guarantee" PMAY approval. The application is free, the portal is public, and no intermediary has influence over the outcome. This is one of the most reliably fraudulent corners of the Indian property market.

The Stamp Duty Question

PMAY does not exempt buyers from paying stamp duty. The former is a central housing scheme, while the latter is a state levy and operates independent of the other.

Some states also offer their discounts that may be available to PMAY beneficiaries on a standalone basis. For instance, Karnataka has stamp duty concession on affordable houses – 3% from ₹21 lakh to ₹45 lakh, 2% below ₹20 lakh. As the PMAY-U 2.0 is capped at ₹35 lakh per house value, most beneficiaries' units in Karnataka will fall within this concession.

Budget stamp duty separately. With rates of 5%–8% of property value in most states, for a ₹35 lakh property, it comes to ₹1.75 lakh to ₹2.8 lakh, exceeding the highest of ISS subsidy, ₹1.80 lakh.

The subsidy doesn't cater to the cost of obtaining the title. Homebuyers who assume that PMAY covers their registration costs will be surprised to find out about that at Sub-Registrar's office.

If you need to find out which micro-markets have properties under the ₹35 lakh cap, our locality guides contain information about price range, connectivity, and availability of the affordable segment properties. Buyers looking for options in NCR usually start with Sector 12 Gurugram

Why Applications Get Rejected

Household income wrongly calculated. The applicant stated their salary but did not mention that of their spouse.

Pucca house not disclosed. Deduplication through Aadhaar reveals it. Same with the title search by the lender.

Wrong carpet area. Built-up was verified rather than carpet area.

No female owner in EWS/LIG. No compromise on this criteria beyond the exemption.

Property located in non-statutory town/non-notified planning area.

Benefit from previous scheme. Only one benefit to one household in lifetime.

Incorrect Aadhaar details. Different names for Aadhaar, PAN, and property records.

Submitted under a closed vertical. Applications under PMAY-U 1.0 CLSS are now closed. Yet some are still applying.

The Documentation Discipline

The self-declaration of non-ownership is the most risky piece of paper that comes along with the deal. It is made with little thought and has actual consequences – recovery of the subsidy with interest, and maybe prosecution for the false declaration.

Before making it, be sure that you do not own the house. Check with your parents if your name is registered anywhere as a landowner. Ask your spouse. Read through the last will if there was any death in the family. You should know that if you have an undivided share in any ancestral property then it's yours and it would appear in revenue records under your name.

This is also true when it comes to the documents of purchase. The moment you make the decision is not the same as when you buy the property. This difference is discussed in detail in our Sale Deed vs Sale Agreement Guide.

The Bottom Line

Eligibility of PMAY in 2026 depends on four criteria and you have to satisfy all four. Households having an annual household income up to ₹9 lakh. Having no pucca house under their name anywhere in India. Carpet Area within the ceiling limit, calculated according to carpet area and not marketed area. A female member in the name of ownership for the EWS and LIG.

The amount of subsidy will be only up to ₹1.80 lakh, under ISS scheme that will be released after 12 years and not immediately. This is less attractive as compared to its predecessor CLSS and even lower than stamp duty charges paid to buy that house.

But none of them are the reason to ignore it. They are just the reasons to make sure about your eligibility before making the house buying plan around it. And you should budget the duty separately from the scheme, as the scheme never was to cover those charges.

Apply through the portal. Apply through the lender. Don’t pay any consultancy fee to anyone. And sign the non-ownership declaration after reading it carefully.

Frequently Asked Questions

1. Is PMAY still available in 2026?

PMAY-U 2.0 is active as per the approval in August 2024, with a budget of ₹10 lakh crore for one crore families in five years. The PMAY-U 1.0 scheme closed for new registrations on 31st December 2024, while the CLSS scheme of the same had expired some time ago. Any guide you find with reference to MIG II slabs and ₹2.35 lakh subsidy has become outdated.

2. What are the income limits for PMAY eligibility?

According to PMAY-U 2.0: EWS up to ₹3 lakh per annum, LIG ₹3-6 lakh per annum, MIG ₹6-9 lakh per annum. The upper limit for MIG has seen a sharp drop. The previous bifurcation between MIG I and MIG II up to ₹18 lakh is not applicable anymore.

3. Is the income limit on my salary or the whole household?

All members of the household – the applicant, his spouse, and his unmarried children, whether their incomes are from renting, farming, interests, or any business activity. Even two people making ₹5 lakhs each make up an annual household income of ₹10 lakhs and are above the limit set for MIG, although they are both in LIG individually.

4. I own a share in my father's ancestral house. Am I disqualified?

Absolutely. It’s based on whether any family member has a pucca house in any part of India, and an inherited share is enough. Even though you have never lived in the property and probably haven’t been to the place in the last ten years, it shows up in the revenue documents with your name.

5. Does owning land disqualify me?

Not at all. The possession of unoccupied land without any pucca structure does not make you ineligible for the program. On the contrary, the Beneficiary-led Construction vertical has been specifically designed for people who possess a plot of land and wish to construct on it, with an upper limit of assistance of ₹2.5 lakh from the center.

6. Does the property have to be in a woman's name?

Yes, under EWS and LIG, the property must be owned or jointly owned by an adult female of the family. This is a mandatory condition and not a choice one, with exceptions made only when there is no adult female within the family. Under MIG, however, the condition is waived and sole male ownership is allowed.

7. How much subsidy will I actually get?

Upto ₹1.80 lakh through Interest Subsidy Scheme – 4% on first ₹8 lakh of loan amount upto ₹25 lakh, on houses worth ₹35 lakh maximum. However, important to note here is that unlike CLSS in version 1.0, it is distributed in five yearly installments over a period of 12 years through push button.

8. My flat is 1,200 sq ft. Does it qualify?

That completely depends upon the nature of the calculation. Caps are calculated based on carpet area. EWS: 30 sqm; LIG: 60 sqm; MIG: 120 sqm. A carpet area of 120 sqm corresponds to a super built-up area of about 175-190 sqm, which equals 1,900-2,050 sq ft. This is the way in which the project measures, while developers market the super built-up area.

9. Does PMAY cover my stamp duty and registration?

Not necessarily. The PMAY scheme is a national level subsidy scheme while stamp duty is an individual state tax that functions independently. For a house valued at ₹35 lakhs, stamp duty and registration cost 5%-8%, costing ₹1.75 lakhs to ₹2.80 lakhs, which is higher than the maximum subsidy amount of ₹1.80 lakhs. There are individual state level schemes that can be looked into. For example, Karnataka levies a 3% stamp duty between ₹21-45 lakhs and 2% below

10. Should I pay a consultant to get my PMAY application approved?

Not necessarily. Since the process is free, the portal is open for everyone (https://pmay-urban.gov.in), and there is no middleman who can manipulate the result, anyone demanding money to "ensure" your acceptance is simply ripping you off — one of the most consistently dishonest areas of the Indian property market. Go to the portal; go through your bank; don't pay anyone.